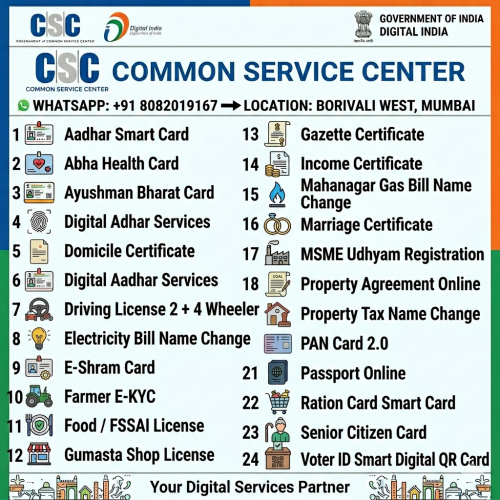

CSC Center is your trusted, all-in-one Digital Seva Kendra, dedicated to eliminating long queues and simplifying government, business, and legal documentation. We provide fast and reliable assistance for essential digital identity management, official state certificates, and crucial welfare scheme enrollments like Ayushman Bharat and E-Shram. From handling comprehensive business compliance—such as MSME, Food/FSSAI, and Gumasta licensing—to processing online passports, driving licenses, and official utility bill name updates, our expert team ensures your paperwork is completed seamlessly, accurately, and efficiently.

Aadhar Smart CardGazette CertificateAbha Health CardIncome CertificateAyushman Bharat Card

Mahanagar Gas Bill Name ChangeMarriage CertificateDomicile CertificateMSME Udhyam RegistrationDigital Aadhar ServicesPAN Card 2.0Driving License 2 + 4 WheelerPassport OnlineElectricity Bill Name ChangeProperty Agreement OnlineE-Shram CardProperty Tax Name ChangeFarmer E-KYCRation Card Smart CardFood / FSSAI LicenseSenior Citizen CardGumasta Shop LicenseVoter ID Smart Digital QR Card

MHADA Housing Lottery Online Application Help

Property

2026-06-08

Rupesh Tanna Blog

Looking for a secure and affordable way to own your dream home in Mumbai? The official MHADA Housing Lottery Portal (housing.mhada.gov.in/landing) serves as the centralized digital platform for the highly anticipated Maharashtra Housing and Area Development Authority (MHADA) lottery schemes.Designed to ensure maximum transparency.

This portal allows homebuyers from across Maharashtra to complete their profile registration, upload mandatory documents via DigiLocker, select their preferred housing scheme, and seamlessly track lottery results.Catering directly to all income slabs—from the Economically Weaker Section (EWS) to the High Income Group (HIG)—the system streamlines the path to secure government-backed, subsidized properties in prime residential locations.Bookmark the landing page today to stay updated on the latest application deadlines, provisional lists, and computerized draw announcements!

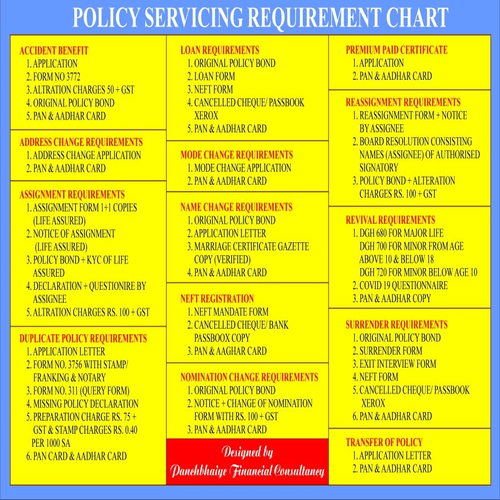

Documents Required for Policy Update or Servicing

Insurance

2026-05-19

Rupesh Tanna Blog

Following Documents Required for Policy Update or Servicing

Accident Benefit

Address Change

Assignment of Policy

Duplicate Policy

Loan Requirement

Mode Change

Name Change

Neft Registration

Nomination Change

Premium Paid Certificate

RE Assignment of Policy

Revival Of Policy

Surrender Of Policy

Transfer Of Policy

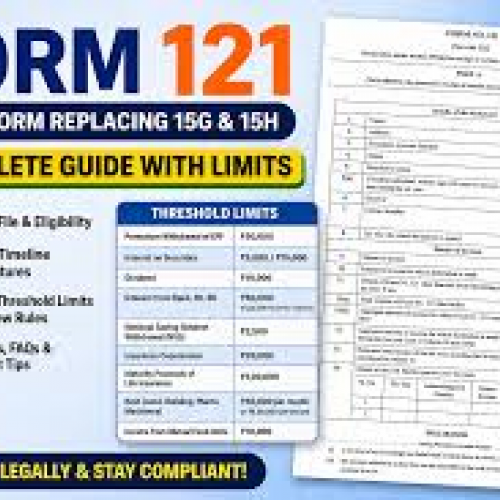

How to fill form 121 of income tax for No TDS as per income tax website

Taxation

2026-05-06

Rupesh Tanna Blog

Form 121 (formerly 15G/15H) is a

self-declaration to avoid TDS on interest, dividends, or EPF withdrawals,

submitted directly to the payer (e.g., bank, EPFO). Fill Part A with PAN,

estimated income, and tax details. Submit via the payer's online portal or

download from the Income Tax Department website. [1, 2]

Note: Submission of this form does not make

income tax-free, it only prevents TDS deduction if total taxable income is

below the threshold. [1]

A Guide to Census 2027: How to Use the Self-Enumeration Portal

General

2026-05-01

Rupesh Tanna Blog

The Census of India 2027 has introduced a digital-first approach, allowing households to complete their registration online. This process, known as Self-Enumeration (SE), is designed to be convenient, secure, and efficient.

If you are planning to register your household, follow this step-by-step guide to ensure your data is submitted correctly.

Please note that the portal is active daily from 6:00 AM to 12:00 Midnight.

State Selection : Select your State/UT and enter the Captcha.

• Household Details: Enter the Name of the Head of Household.

Note: The Name of the Head of Household cannot be changed once the registration is initiated.

• Contact Information: Enter your 10-digit Mobile Number and an optional Email ID.

o Rule: Only one mobile number can be used per household. Once registered, this number cannot be used for any other household registration.

SECTION 2: Verification and Location Identification

After the initial registration, you must verify your identity and pin-point your residence on the digital map.

• Language Selection: Select your preferred language for the questionnaire.

o Warning: The selected language cannot be changed later in the process.

• OTP Verification: Enter the OTP sent to your registered mobile number to verify your session.

• Address Details: Select your District and enter your PIN code, Village, Town, or Locality.

• Map Marker: Drag the Red Marker on the interactive map to identify the exact location of your residential building and click "Confirm Location."

SECTION 3: Data Entry and Final Submission

In this final phase, you will provide the specific details required for the housing census.

• Completing the Questionnaire: Fill out the Housing Census Questionnaire. You can use the built-in Tooltips, FAQs, and "Essential Information" notes if you have questions about specific fields (such as floor material, drinking water sources, or ownership status).

• Preview and Edit: Use the Preview Screen to review all entered data. You may edit entries or save a draft to submit at a later time.

• Final Submission: Once you are satisfied with the accuracy of your data, click "Submit."

o Crucial: No changes can be made to your data after the Final Submission.

Post-Submission: The SE ID

Upon successful submission, a unique 17-digit SE ID (prefixed with the letter 'H') will be generated. This ID will be sent to you via SMS and Email (if provided).

What to do when an Enumerator visits?

When a Census Enumerator visits your home, simply share your SE ID with them.

• ID Match: If the SE ID matches the existing digital record, your details are confirmed and the process is complete.

• No Match: If the ID does not match, the Enumerator will collect the data afresh to ensure your household is correctly recorded.

Stay Updated: For state-wise self-enumeration periods, please check the "SE Period" section on the official portal to ensure you complete your registration before the deadline.

Why You Must Secure Your Retirement Income Before Interest Rates Fall Further

Financial Planning

2025-06-06

Rupesh Tanna Blog

The Reserve Bank of India (RBI) recently reduced the repo rate to 5.5%, a step taken to revive economic growth and enhance credit availability. While this move may support borrowing and business activity, it poses a silent challenge to conservative investors especially retirees and those dependent on fixed-income instruments.

As repo rates trend downward, bank fixed deposit (FD) rates and pension returns are also expected to decline, since they’re closely linked. If you're relying on traditional savings tools like FDs or conventional pension plans for your future income, this shift could erode your financial stability over time.

The Silent Threat of Falling Interest Rates

Most investors view fixed deposits and pension plans as "safe" options. While they may be safe in terms of capital protection, they’re not immune to interest rate fluctuations. A falling interest rate environment leads to:

Lower returns on reinvested fixed deposits

Reduced pension income from rate-linked plans

Erosion of purchasing power due to inflation

In such a scenario, it’s critical to diversify your retirement corpus and ensure that at least part of your income is protected from future interest rate cuts.

Jeevan Akshay and Jeevan Shanti: Your Shield Against Falling Returns

LIC of India offers two powerful annuity plans "Jeevan Akshay and Jeevan Shanti" that act as lifelong financial shields in uncertain times.

Key Benefits:

Guaranteed Lifetime Income: Once locked in, your income remains stable, irrespective of market or interest rate changes.

Interest Rate Immunity: Your returns are fixed at the time of purchase and are unaffected by falling repo or FD rates.

Trusted Backing: These plans are issued by LIC, India’s most trusted life insurer, with sovereign backing and long-term credibility.

Flexibility: Options for single life, joint life, deferred annuity, and more based on your retirement goals.

Why Act Now?

With further repo rate cuts likely in the near future, delaying your investment could mean locking into lower annuity rates. Acting now allows you to lock in higher lifelong income while current rates are still relatively favorable.

Ready to Take Control of Your Financial Future?

If you're looking for stability in uncertain times, LIC’s Jeevan Akshay and Jeevan Shanti plans offer a reliable, tax-efficient, and stress-free solution for retirement planning.

Feel free to reach out to learn more about how these plans can fit into your financial strategy.

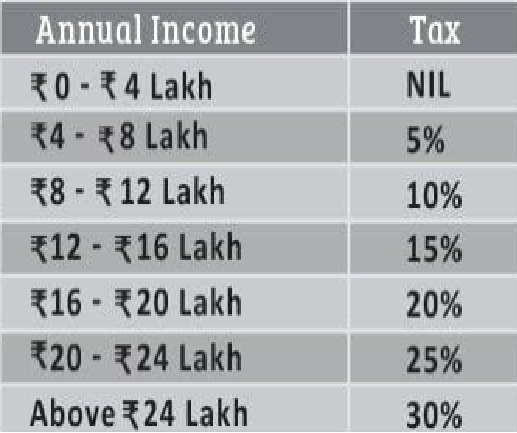

Major Highlights of Budget 2025

Budget

2025-02-01

Rupesh Tanna Blog

NEW TAX REGIME

Zero Income Tax for Annual Income up to Rs 12Lakh

No Income Tax Upto Rs 12.75 Lakh for salaried Taxpayer with a standard deduction of Rs 75,000

Taxation: No tax up to ₹12 lakh (new regime), relief for higher incomes, simplified slabs/TDS/TCS, higher LRS threshold (₹10 lakh), increased rent TDS threshold (₹6 lakh), no TCS on education loans (up to ₹10 lakh). New tax bill.

Today (30th October) is World

Savings Day, A Special Day which re-emphasizes the importance of savings in our

day to day life. Right from our childhood, We have been taught that `A Penny

Saved is A Penny Earned`. The Phrase highlights the importance of savings which

is an proven way for Financial Success.

Here are few reasons why savings is necessary

for everyone.

Wealth Creation: When you save and invest your money, you are putting your money at work to create more money. This is a proven way for wealth creation.

Protection Against Emergencies: In today`s world nobody can predict what lies ahead. But by saving money anyone can be prepared for the future. When you save money, you are creating a contingency plan

for unforeseen Financial or Medical issues.

Retirement Planning: Retirement Planning is not a short term goal. It requires regular and disciplined savings for long term. By saving your money, you can ensure a hassle-free retirement without worrying

about money.

Achieving Financial Goals: When you save regularly, you need not compromise on your financial goals and can achieve them easily without falling for the trap of loans at higher interest rates.

Every Woman Deserves Financial Freedom

Financial Planning

2023-03-08

Rupesh Tanna Blog

In every growing society, women are back bone of it and we are proud to say that we play a small part in strengthening the back bone by helping women become financially empowered.

First step of financial empowerment begins when we guide parents to make an investment in their daughter`s name so that she has a corpus to rely upon in case of any misfortune happening or despite it. Every girl today should have some wealth in her name as she reaches adulthood.

Second step we take is to help young women understand why it is important to invest money and save for themselves. With growing economy, more and more private sector jobs are opening up which on one hand is good but it also means no retirement pension from government.

So it`s imperative that every girl has a retirement plan for herself.

Third step is to guide every young man to make their wife nominee in all the investment they make and most importantly involve his wife in all the decisions. Wife should always be aware of any investment made so that in case any of any misfortune, she can handles it on her own and doesn`t have to rely on anyone.

With these three steps we make sure that all the women who come in contact with our firm directly or indirectly have a legacy in her name.

We invite you to be a part of our mission and help us by educating women and making them self-dependent on anything financial. A financially self-dependent woman creates a strong family and society.